PUR increases JORC lithium resource by 339%

Our Argentine lithium brine Investment Pursuit Minerals (ASX: PUR) has just increased its resource by 339%.

PUR’s resource now stands at ~1.1 million tonnes of LCE (Lithium Carbonate Equivalent).

PUR also managed to increase the grade of its resource too - the average lithium concentration across its resource is now 505.8mg/li.

(Previously, the concentrations were ~351mg/Li).

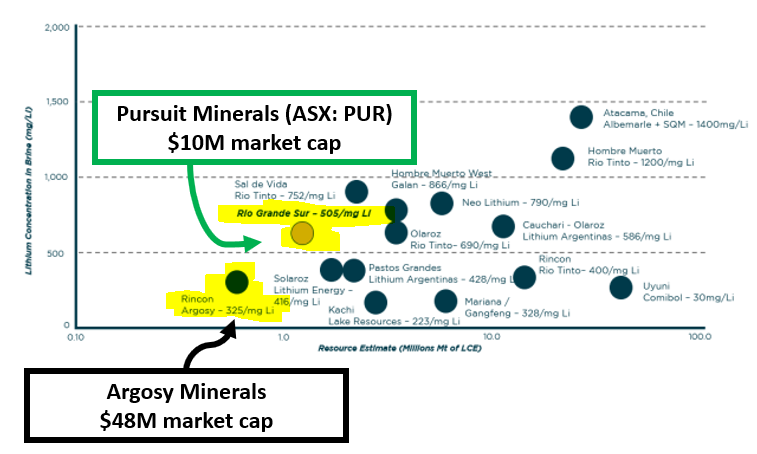

After today’s news we think PUR has given the market a pretty good standard by which to compare its project to other ASX listed brine players.

The most obvious comparison is Argosy Minerals which is progressing its brine asset in blah.

Argosy are more advanced than PUR having already developed a 2,500tpa demo project BUT Argosy’s resource is smaller and a lot lower grade.

Grade and size matter when it comes to lithium brine projects because it typically means lower operating costs and more economies of scale once at full production capacity.

Argosy’s resource is ~731.8kt LCE and the company is capped at ~$48M.

PUR’s resource is bigger (~1.1Mt LCE) and is currently capped at ~$10M.

PUR can increase its resource further:

We note there is still plenty of scope for PUR to increase its resource further.

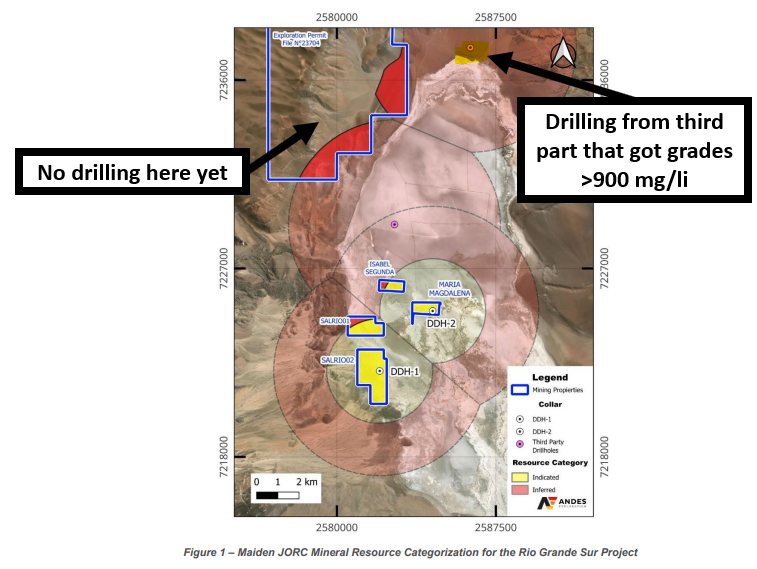

PUR has only drilled two holes on its project and is yet to drill its biggest project (Mito) which sits on the northern fringes of the Rio Grande Salar.

That northern fringe is where nearby operators have hit grades in the 900’s Mg/Li.

We think that with some deeper drilling inside the Salar & with a drill program on Mito, PUR could increase its resource even further.

Why we think the resource upgrade matters

First of all it sets a reference point for PUR’s project to be compared to other companies with similar projects.

I.e the market can calculate and then extrapolate $/ tonne of LCE calculations across companies with brine projects in South America.

Second - it means PUR can move the project into the feasibility study stage based on the much larger resource (and improved grades).

Feasibility studies with projects like this are important because it can give investors a set of financials to start to think about the potential of the project under a set of different assumptions.

I.e investors can see how the project stacks up at today’s lithium prices and how it might stack up if prices were 2-3-4x of where they are now.

It also allows for any gaps between a company’s on market valuation and the underlying value of a project to be bridged.

In PUR’s case we think the company’s current valuation has a lot to do with the broader macro sentiment in the lithium space and so going back to studies could be a good idea.

While on market valuations have been hit pretty hard across the lithium space, there is still corporate interest in projects across the world so giving investors a set of financials may help set a price floor for the company’s share price.

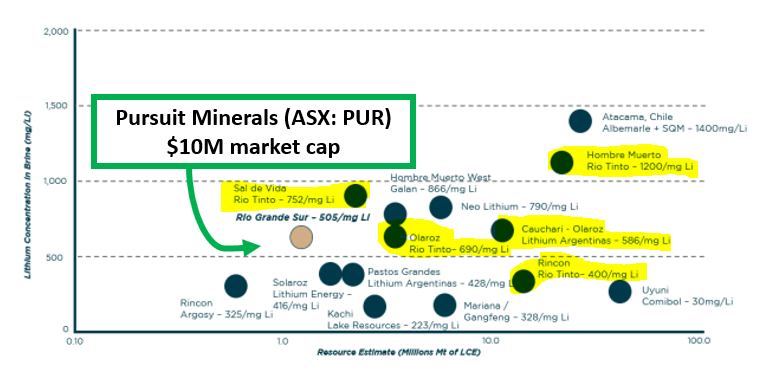

Of note is the big Arcadium Lithium purchase by Rio Tinto in a deal worth ~US$6.7BN.

A big part of the Arcadium portfolio is a set of lithium brine assets in Argentina…

Here are some of the Rio owned assets on that resource comparison table from earlier:

Arcadium is a completely different beast to PUR, it has other business streams outside of its brine assets BUT we think the Rio deal is a good sign that corporates are still very much interested in the lithium sector as a whole based on a longer term view of things.

What’s next for PUR?

Commissioning of pilot plant 🔄

In today’s announcement, PUR mentioned that future works would be focussed on getting the companies 100% owned 250tpa pilot plant commissioned.

PUR also made mention of “ongoing discussions with potential off-take partners and end users” which we think will unlock the pilot plant.

First though, PUR needs to get all of the permitting complete for its evaporation ponds.

In the short term we are hoping to see two things:

- Some sort of commercial deal that speeds up commissioning of the plant.

- Permitting on the evaporation ponds & development work PUR needs to do to turn its brines into LCE.

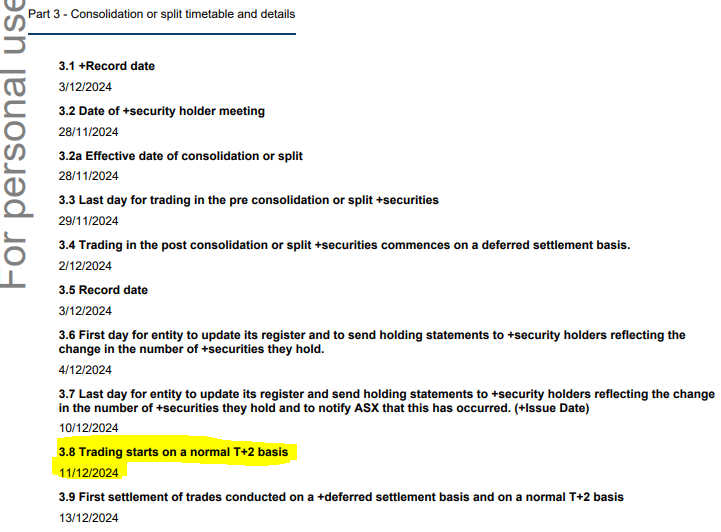

Completion of consolidation 🔄

We also want to see PUR complete its consolidation and start trading under its normal ticker (PUR).

The 50:1 consolidation process is expected to be completed on the 11th of December so we should start to see more normalised trading in the company then.

(Source)